FTX Modifies Bitcoin And Crypto Sale Proposal Last Minute

In a recent court filing, FTX, the crypto exchange currently navigating bankruptcy, has made last-minute adjustments to its proposal concerning the sale of its Bitcoin and crypto holdings. This move is seen as an attempt to address concerns raised by the US Trustee, the bankruptcy branch of the Department of Justice.

FTX’s initial proposal, which is set to be reviewed in a Delaware Bankruptcy Court today, September 13, aimed to liquidate $3.4 billion in Bitcoin and other crypto assets. The market had been rife with concerns about the potential impact of such a massive sale, fearing it could exert significant selling pressure on an already fragile market.

On August 24, FTX had proposed appointing Galaxy Digital, led by Mike Novogratz, as the investment manager to oversee the sale and management of these recovered assets. The plan allowed FTX to sell up to $100 million worth of tokens per week, a cap that could be increased to $200 million on an individual token basis.

Details Of The Revised Bitcoin And Crypto Sale Proposal

FTX’s revised proposal indicates that the exchange will not be required to issue advance public notice of these transactions due to their potential to significantly influence market prices. This decision comes in light of the fact that the mere prospect of a crypto entity selling up to $100 million of assets weekly has already dampened the sentiment of the market.

The US Trustee had initially opposed FTX’s plan, emphasizing that any intent to sell off significant assets like bitcoin (BTC) or ether (ETH) should be widely publicized to allow others the opportunity to voice objections. In a compromise, FTX has now agreed to keep the US Trustee and committees representing the exchange’s creditors privately informed.

FTX’s holdings, as of August 31, include $1.16 billion in Solana’s SOL, $560 million in BTC, $192 million in ETH, $137 million in APT, $120 million in USDT, $119 million in XRP, $49 million in BIT, $46 million in STG, $41 million in WBTC and $37 million in WETH.

Notably, a significant portion of FTX’s SOL tokens is locked and will only be fully vested between 2025 and 2028. This means any sale would involve a buyer taking over FTX’s vesting contract, negating the possibility of a sudden massive dump of SOL tokens.

Market Reactions And Concerns

Renowned crypto trader Hsaka voiced concerns on X about the potential information disparity. Hsaka pointed out that while market makers and OTC buyers might receive crucial price-moving information, smaller investors could be left in the dark. He tweeted: “So with the new FTX liquidation proposal they wouldn’t issue advanced public notice before they start liquidating assets, but would let members of the creditors committee know. The same committee with a bunch of Market Makers and OTC desks on it?”

While FTX’s last-minute changes to its liquidation plan seem strategic, aiming to minimize potential market disruptions, they also raise questions about transparency. The court order authorizing the liquidation still suggests that the interests of all stakeholders have been considered. However, the Bitcoin and crypto community will be keenly watching Judge John Dorsey’s decision in the Delaware courtroom and the subsequent market reactions.

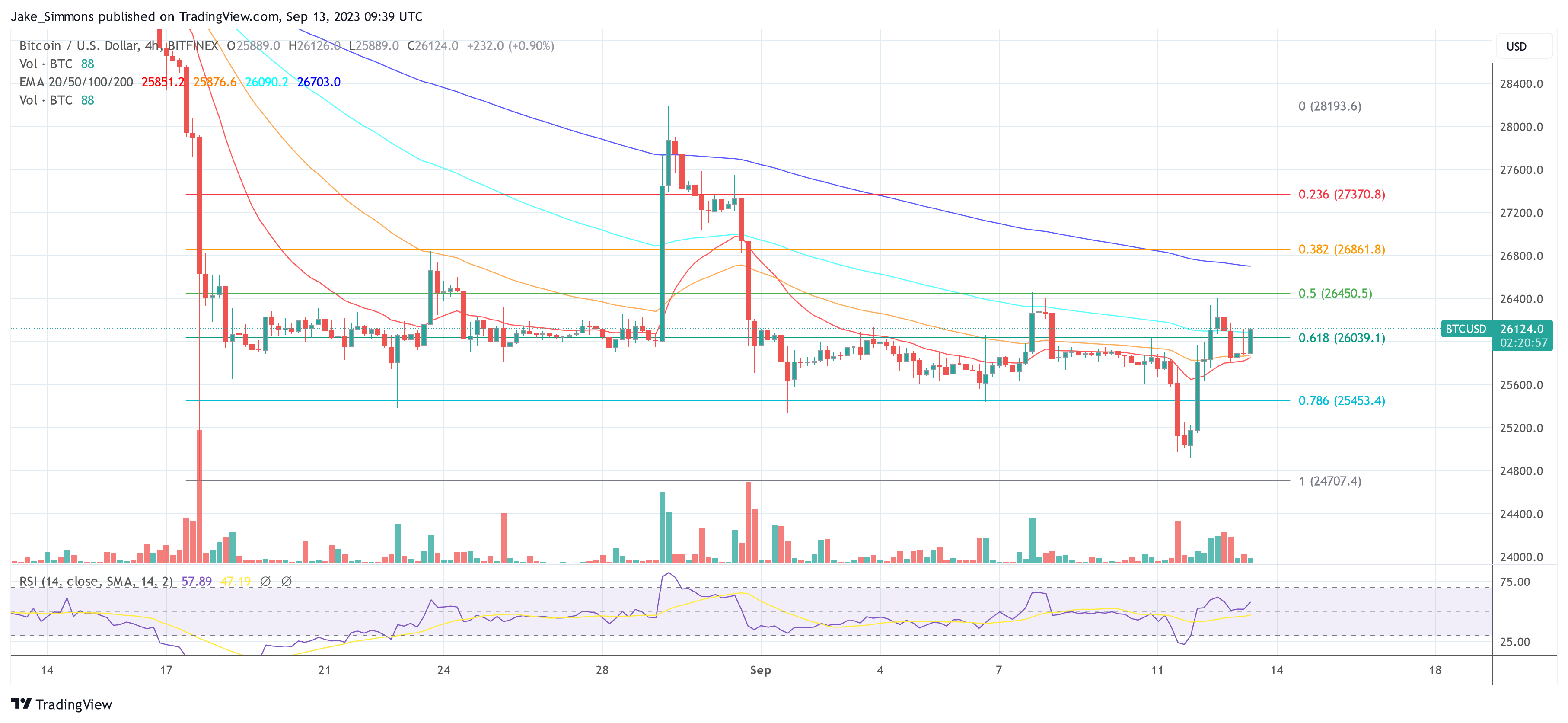

At press time, BTC traded at $26,124.

Featured image from The Conversation, chart from TradingView.com